I was reading through below mentioned article and thought of sharing with the readers of this blog. The content of the article is very relevant in todays market situation. To read the original article, click here.

India’s GDP growth has been hitting new lows primarily due to collapse in the investment cycle. Investment gurus and TV pundits are urging investors to increase allocation to equities suggesting that the investment cycle is close to bottoming out and is all set for a strong rebound. However there is another cycle namely the ‘Investor behaviour cycle’ which tends to have an even greater impact on the end returns an investor eventually makes.

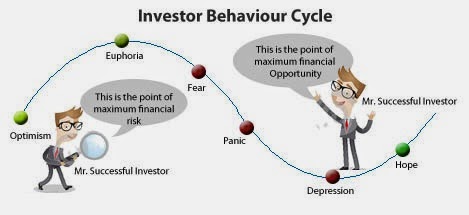

A typical investor behaviour cycle starts with optimism driven by a change in the environment. Investors allocate some savings to equity hoping to make positive returns. As more and more investors start investing in equity their return expectations are realised as the market continues to move higher. With return expectations met, recency bias kicks in (extrapolating most recent events into the future, in this case positive returns). Investors not only reinvest their original savings and returns but in fact increase allocation by putting in more savings (in some cases using leverage). This phase coincides with euphoria as the market starts hitting new highs. One sees a host of equity issuances as promoters lap up the opportunity to raise cheap equity. Risk is thrown out the window and the rising tide of liquidity lifts all boats, money making becomes extremely easy. All investors start believing they are investment geniuses, as any stock they invest in, is up 25% in a week with a lot more upside to go. All this continues till an event in the environment forces people to start looking at risk again. As investors book profit share prices tumble and as more and more people start selling, the cycle in reverse this time, reinforces itself.

Here is a graphical representation of investor behaviour ... as it is :

In India’s case a weak multi party coalition being replaced by a strong single party majority was a reason to be optimist. We have seen a sustained rally in equities since August 2013, firstly driven by anticipation of a change in government and then in hope of potential structural reforms initiated by the new government. The early optimism seems to have now reached a stage of euphoria as a host of penny stocks hit circuit filters every day. New issuances which had dried up over the last three years suddenly have resurfaced primarily via the QIP market (a lot of them by companies tethering near bankruptcy which have been thrown a lifeline). The IPO market will start buzzing sooner rather than later. Downside risk is a term not heard often.

How long this euphoria lasts is anyone’s guess. But we do know that expectations in the market are running high with risk averseness running low. Investors would be well advised to ignore all this noise and focus on fundamentals alone. A stock specific approach focusing on company’s long term earnings potential evaluated against its risk is well advised (which is the process followed by Quantum Long Term Equity Fund*). Everything else is best ignored.

Also, when it comes to your investments, your redemption should depend on your financial goals. A mere guess should not hamper your investments and your potential to earn better returns. As an investor you should also consult your financial advisor before taking an important investment decisions.

No comments:

Post a Comment